Economic and Political Outlook for North America, 2024-2025

United States Economic Resilience Amidst Global Uncertainty

The United States economy is anticipated to exhibit robust resilience, propelled primarily by steady consumer spending. Real GDP growth is forecasted to reach 2% for 2024, with a slight deceleration to 1.6% in 2025. This positive economic outlook is underpinned by sustained household expenditure, bolstered by full employment and the prevalence of long-term fixed-rate mortgages that shield most homeowners from the interest rate hikes of 2022-2023. While private consumption growth is expected to dip marginally, the slowdown in GDP growth from 2.5% in 2023 can largely be attributed to reduced government consumption and a weaker external sector contribution. However, fixed investment is set to accelerate, driven by industrial incentives and a recovery in the housing market.

Canadian Economic Growth Bolstered by US Demand

Canada’s economic expansion is forecasted to reach 1.9% in 2024, an improvement from 1.1% in 2023, with further acceleration expected in 2025. The resilience of the US economy, coupled with robust global commodity demand, will support Canadian growth. However, the exposure to the property sector, characterized by medium-term mortgages requiring refinancing at higher interest rates, will remain a constraint.

Atypical Recession Avoidance in Historical Context

The forecasted moderate slowdown in the US economy, despite the Federal Reserve’s aggressive policy tightening, marks an unusual deviation from past cycles. While tighter monetary policy has had notable impacts—evident in the failure of some regional banks, reduced public share offerings, and the collapse of speculative assets—robust job growth and strengthened household finances, aided by enhanced financial regulations post-global financial crisis, have mitigated a larger economic downturn.

Adjustments in Federal Reserve Policy

Despite fluctuations in US inflation, it is anticipated that consumer price increases will align with the Federal Reserve’s 2% target by the latter half of 2024, as rental cost inflation subsides. Consequently, the timeline for the Federal Reserve to reduce its policy rate has been extended to September 2024, with an expected 50-basis-point reduction by year-end, lower than previously anticipated. The policy rate is forecast to remain above the pre-pandemic average, influenced by a tighter labor market and elevated input costs due to supply-chain shifts. Canadian inflation and interest rates are projected to mirror those in the US.

Legislative and Political Risks

The US faces high domestic political and policy risks through 2024-25, exacerbated by challenges in securing annual federal funding and recent debt ceiling standoffs. With a divided Congress—Republicans controlling the House and Democrats the Senate—the prospects for advancing new legislation remain bleak ahead of the November 2024 elections. The administration will focus on implementing previously passed bills, such as the CHIPS and Science Act and the Inflation Reduction Act (IRA), which have spurred industrial investments. If re-elected, the current administration will prioritize climate transition and industrial policies, though elements of the IRA may face challenges under a Republican administration. Regardless of the election outcome, strategic incentives for domestic and regional production of key technologies will persist, driven by US-China competition.

Electoral Outlook

The forthcoming presidential race is anticipated to be highly competitive. Although the current president is forecasted to secure re-election, his approval ratings are low, and he has lost ground in key swing states. Nonetheless, strong employment figures, rising real wages, and a well-funded campaign may bolster his support. The Democrats are expected to consolidate against the presumptive Republican nominee, who faces challenges in garnering moderate and independent voter support due to ongoing legal issues and controversial stances on key issues.

Geopolitical Strategy and Challenges

The US will leverage its economic, financial, and military strengths, alongside reinforced alliances, to maintain its global dominance amidst escalating geopolitical competition. The strategic rivalry with China will heavily influence US foreign policy, focusing on technological and industrial competitiveness and deterrence of Chinese military actions in Asia. Concurrent geopolitical demands from the Middle East and the Russian invasion of Ukraine will test the US’s ability to concentrate on China. The administration aims to reduce US involvement in the Middle East to prioritize this focus, whereas a different administration might shift the focus to Ukraine.

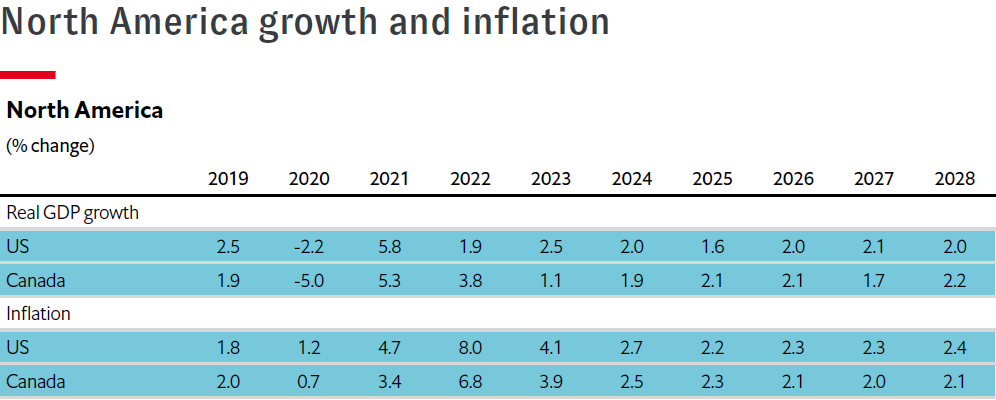

Comprehensive Economic Indicators and Projections

The North American region’s economic outlook presents a detailed picture of anticipated growth rates and inflation trends over the next few years. The US is projected to maintain a real GDP growth rate of 2% in 2024, which will moderate to 1.6% in 2025, followed by slight fluctuations through 2028. Inflation is expected to stabilize close to the Federal Reserve’s target, settling at 2.7% in 2024 and further reducing to around 2.2-2.4% in the subsequent years.

Canada’s economy, similarly, is expected to experience steady growth. After a significant recovery post-2020, the GDP growth rate is projected to be 1.9% in 2024, accelerating to 2.1% in 2025, with a slight dip and subsequent recovery through 2028. Inflation rates in Canada are forecasted to align closely with those in the US, stabilizing around 2.0-2.5% from 2024 onwards.

Strategic Industrial Policies

A key area of bipartisan consensus in the US remains industrial policy, particularly in response to the strategic competition with China. The continued implementation of the CHIPS and Science Act and the Inflation Reduction Act is expected to drive significant public and private investment into the industrial sector. These policies aim to bolster US technological and industrial capabilities, particularly in areas such as semiconductors, renewable energy, and electric vehicles. This reindustrialization push is anticipated to support economic growth and enhance the country’s competitive edge on the global stage.

Conclusion

In conclusion, North America’s economic landscape for 2024-2025 will be shaped by the interplay of resilient domestic growth, strategic industrial policies, and complex geopolitical dynamics. While the US and Canadian economies are projected to experience moderate yet steady growth, the political environment remains fraught with challenges. The foundational economic strengths and strategic imperatives will guide the region’s trajectory in the near term, with industrial policy and geopolitical strategy playing crucial roles in shaping the future. The overall outlook, while cautiously optimistic, acknowledges the potential headwinds posed by domestic political uncertainties and global geopolitical tensions.

US Hits China with Carefully Devised Tariffs

Context and Background

The geopolitical landscape between the United States and China continues to be fraught with tension, despite efforts at bilateral engagements in recent months. On May 14th, the United States Trade Representative (USTR) unveiled a strategic imposition of tariffs on approximately USD 18 billion worth of Chinese imports. These measures are an extension of the broader tariff regime originally instituted during the Trump administration under Section 301 of the US Trade Act, following a comprehensive two-year review by the Biden administration. Concurrently, the Biden administration has revoked licenses previously granted to US semiconductor giants Intel and Qualcomm, restricting their ability to export certain chips to Chinese tech behemoth Huawei. Moreover, US lawmakers are advancing a bill aimed at curbing the export of artificial intelligence models to China, further straining tech relations.

Economic Impact

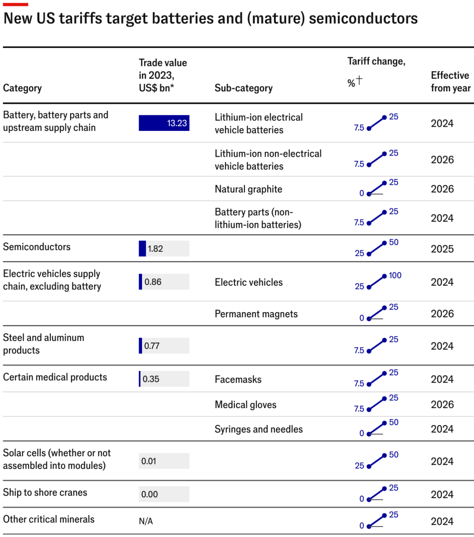

The newly announced tariffs, while covering a relatively small portion (less than 4%) of the total USD 488 billion in US imports from China in 2023, are tactically significant. They are meticulously designed to target sectors that are central to the Biden administration’s domestic economic agenda, which includes substantial investments in domestic manufacturing and clean energy. These initiatives are encapsulated in key legislative frameworks such as the Inflation Reduction Act, the CHIPS and Science Act, and the Bipartisan Infrastructure Law.

Electric Vehicle (EV) Supply Chain Focus A significant proportion of the new tariffs are directed at the electric vehicle (EV) supply chain. This includes lithium-ion batteries, which constitute about 80% of the affected imports. The imposition of these tariffs is expected to create supply chain disruptions for US automakers who rely heavily on Chinese batteries and related components. However, Chinese manufacturers, having anticipated such moves, have been progressively reducing their dependence on the US market, thereby mitigating the impact on their operations.

Strategic Delays and Exemptions To avoid hampering its own strategic initiatives, the US has opted for a phased approach. Several critical inputs necessary for the EV supply chain, including permanent magnets, natural graphite, and specific types of batteries, will not be subjected to tariffs until 2026. Additionally, the USTR has proposed exclusions for 330 categories of industrial machinery, with 19 categories specifically related to the manufacturing of solar components. This selective exclusion underscores a strategic intent to balance trade restrictions with the imperative of advancing domestic industrial capabilities and clean energy objectives.

Political Implications

On the domestic front, these tariffs serve a dual political purpose. They reinforce President Biden’s protectionist stance, appealing to a voter base concerned with protecting and reviving US manufacturing industries. This aligns with broader political narratives focused on reducing dependency on Chinese industrial output and addressing issues related to overcapacity in Chinese manufacturing.

Election Strategy The tariff measures are also part of a broader political strategy in the run-up to the US presidential election. Both President Biden and former President Trump are positioning themselves as strong on China, reflecting a bipartisan consensus on the need to counter Chinese economic practices. Trump’s recent rhetoric, threatening to impose up to 200% tariffs on China-made EVs, though largely symbolic, underscores the competitive political landscape where each candidate seeks to demonstrate toughness on China.

International Repercussions The imposition of these tariffs by the US could catalyze similar actions from other major economies. The European Union, for example, shares the US’s concerns regarding China’s growing dominance in the automotive export sector. The EU is anticipated to introduce its own tariffs on Chinese EVs and other imports, potentially as early as July, following an ongoing anti-subsidy investigation. Such coordinated international measures could signify a broader alignment among Western economies in response to China’s trade practices.

Anticipated Chinese Response

In response to the new US tariffs, China has pledged to enact “resolute measures.” However, it is expected to adopt a measured approach. Historical precedents from 2018-19 suggest that China is likely to introduce reciprocal tariffs targeting a similar value of US imports. These measures are anticipated to have limited broader economic impact, reflecting a strategic choice to avoid escalating trade tensions further.

Preserving Business Environment China is likely to refrain from targeting US firms operating within its borders, maintaining its rhetorical commitment to being open to foreign businesses. This approach is indicative of China’s broader strategy to manage international trade conflicts prudently, especially given its ongoing economic tensions with the EU. Consequently, the current level of trade tensions between the US and China is expected to be more contained compared to the tit-for-tat tariff exchanges during the Trump administration.

Strategic Outlook

The US’s tariff strategy reflects a careful balancing act aimed at reducing China’s influence in critical supply chains while safeguarding its own economic and industrial initiatives. By phasing in tariffs and allowing exemptions, the US aims to mitigate potential disruptions to its own clean energy and manufacturing sectors. This nuanced approach may encourage other economies to adopt similar protective measures against Chinese imports, potentially leading to a more coordinated international stance on trade with China.

The strategic imposition of tariffs highlights the intricate interplay of economic policy and international diplomacy as the US navigates its complex relationship with China. The anticipated restrained response from China suggests a potential stabilization of trade tensions, albeit within a framework of continued strategic competition. This development marks a significant moment in US-China trade relations, with profound political and economic implications shaping the future trajectory of global trade dynamics.

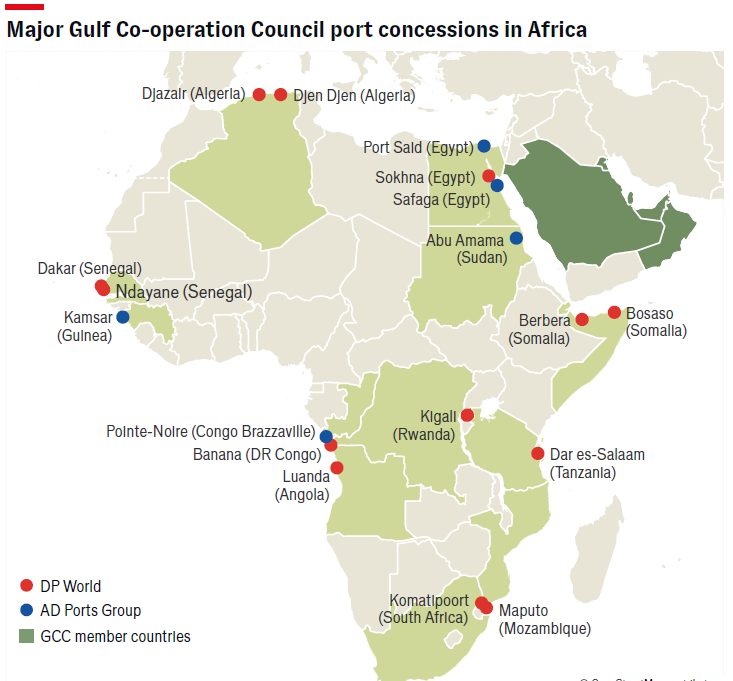

The Gulf Cooperation Council’s Expanding African Footprint

The Gulf Cooperation Council (GCC) states, particularly Saudi Arabia, the UAE, and Qatar, are amplifying their presence and investment across Africa. This burgeoning engagement is evidenced by a significant rise in foreign direct investment (FDI) and trade activities, driven by multifaceted economic and political motivations.

Key Areas of Investment and Expansion

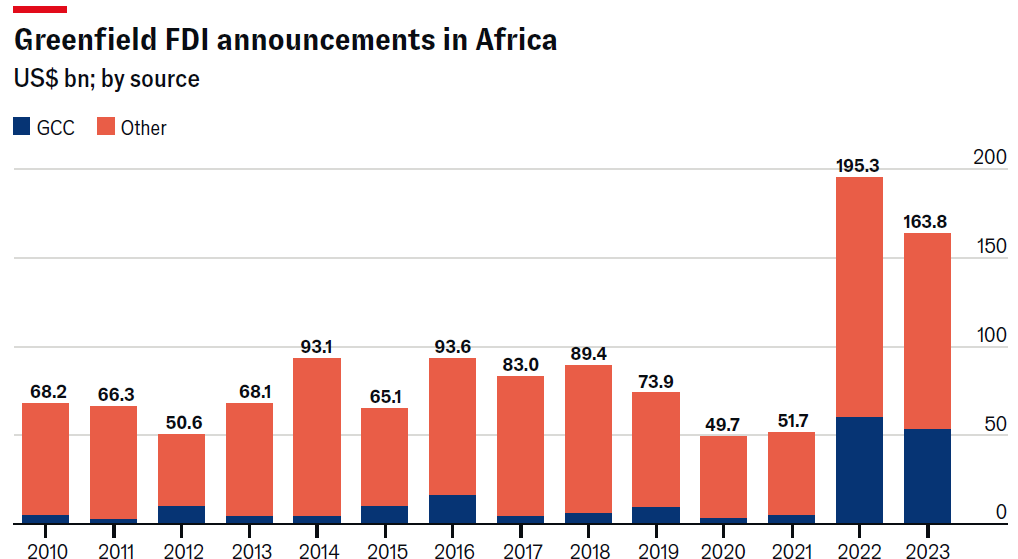

Resource Industries and Infrastructure: GCC investors are heavily investing in Africa’s resource sectors, notably oil and gas, mining, and agriculture. These ventures are complemented by substantial investments in transport infrastructure and logistics services, enhancing the efficiency and connectivity of these industries. In 2022 alone, GCC greenfield FDI announcements in Africa reached a record USD 60 billion, followed by USD 53 billion in 2023. This level of investment surpasses commitments from other major global players, including China, Western Europe, and the United States. The primary targets for these investments include oil and gas extraction projects, agricultural land acquisitions, and mining operations aimed at securing essential minerals and metals.

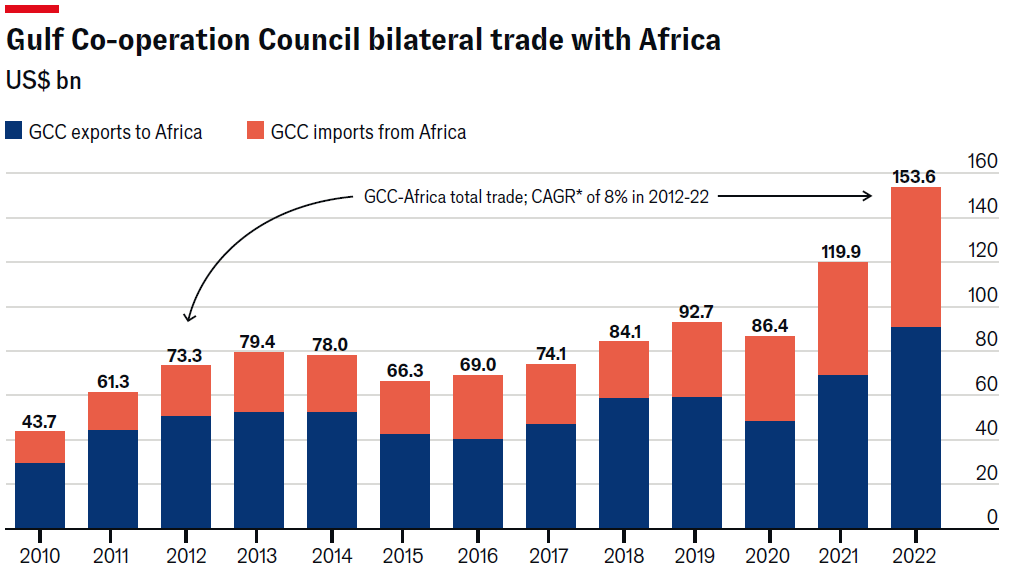

Bilateral Trade Growth: Trade between the GCC and Africa has seen robust growth, with a compound annual growth rate (CAGR) of 8% over the past decade, reaching a record high of USD 154 billion in 2022. This trade volume places the GCC as a formidable trading partner for Africa, outpacing traditional allies such as the US (USD 74 billion) and India (USD 99 billion) and closing the gap with China (USD 289 billion) and Western Europe (USD 244 billion). The core of this trade relationship lies in the exchange of oil and gas from the GCC and mining products from Africa, though diversification is increasingly evident. Non-oil trade is flourishing, underpinned by the GCC’s cumulative investments in Africa’s infrastructure, technology, and renewable energy sectors.

Logistics and Transport Infrastructure: The UAE, through companies like DP World and AD Ports Group, has established controlling stakes in numerous African ports and logistics hubs. These strategic investments aim to secure the UAE’s role in managing key import-export nodes, thereby facilitating increased trade between Africa, the Middle East, Asia, and Europe. Key projects include the management of two-thirds of the Dar es Salaam port in Tanzania and the development of a multipurpose terminal at Safaga seaport in Egypt. These ventures are designed to streamline logistics, enhance trade efficiency, and solidify the UAE’s influence over critical maritime routes.

Natural Resources and Food Security: GCC states are securing stakes in Africa’s hydrocarbons and mining sectors, capitalizing on their financial prowess and expertise. The UAE’s agreement with Morocco to finance the Atlantic gas pipeline project and the development of petroleum storage and distribution facilities across Africa by Abu Dhabi National Oil Company (ADNOC) and Emirates National Oil Company (ENOC) highlight this focus. Investments in agricultural land and food production facilities are pivotal for addressing the GCC’s food security concerns. Countries such as Angola, Egypt, Ethiopia, and Sudan are engaged in or negotiating long-term land lease deals with GCC states, ensuring a steady supply of agricultural produce to the Gulf.

Renewables and ICT: The GCC’s focus on renewable energy is evident, with plans to inject billions into solar and green hydrogen projects across Africa. The UAE’s Masdar aims to mobilize up to USD 10 billion for renewable energy projects, targeting an additional 10 GW of clean energy capacity by 2030. Saudi Arabia’s ACWA Power is actively developing solar energy parks, including the operational 100-MW Redstone project in South Africa. Concurrently, investments in the ICT sector are creating new partnerships and fostering digital transformation, particularly in major markets like Egypt, Kenya, and South Africa. GCC-based companies are engaging in cloud computing, data centers, and fintech initiatives, thereby bolstering Africa’s digital infrastructure and technological capabilities.

Motivations and Strategic Implications

Economic Diversification and Market Potential: The GCC states are positioning themselves to tap into Africa’s fast-growing markets and regional economic communities. Initiatives like the African Continental Free Trade Area (AfCFTA) offer significant future market potential. The GCC’s financial engagement is appealing due to its rapid disbursement and minimal conditions compared to Western financial institutions. This agility in financing is particularly attractive to African nations looking for quick and reliable sources of capital.

Security and Strategic Interests: Improving security in regions like the Red Sea and the Horn of Africa is crucial for the GCC, given its strategic importance for global trade and energy exports. This has led to diplomatic and military engagements, including brokering peace deals and providing aid to stabilize the region. Saudi Arabia and the UAE, in particular, are keen on ensuring the stability of the Red Sea corridor, which is vital for the safe passage of oil tankers and cargo ships. Their involvement includes financial aid, military training, and diplomatic support to governments and factions within these regions.

Soft Power and Diplomatic Engagement: The GCC is extending its soft power through increased diplomatic presence and financial support across Africa. The UAE and Qatar have significantly expanded their embassies, while Saudi Arabia plans to follow suit, enhancing their influence and fostering deeper commercial ties. This diplomatic outreach is not merely symbolic but is backed by substantial economic commitments. For instance, the UAE’s humanitarian efforts in Somalia and financial pledges to Egypt and Ghana illustrate a blend of soft power and economic diplomacy aimed at strengthening bilateral relations.

Future Outlook

Strategic Alliances and Regional Influence: The GCC’s engagement with Africa will continue to blend economic investment with strategic alliances. As Africa undergoes rapid economic transformation, the GCC states are positioning themselves as indispensable partners. They are leveraging their financial resources, technological expertise, and geopolitical strategies to secure long-term benefits. The growing number of Africa-registered companies in Dubai’s Chamber of Commerce, coupled with the establishment of new diplomatic missions, underscores the depth of GCC-Africa ties.

Economic Integration and Infrastructure Development: Future engagements will likely focus on enhancing economic integration and infrastructure development across the continent. The GCC’s investments in Africa’s renewable energy, ICT infrastructure, and transport networks are poised to drive substantial economic growth and technological advancement. These efforts will not only benefit African economies but will also provide the GCC with new markets and opportunities for economic diversification.

Challenges and Opportunities: While the outlook is promising, the GCC’s ventures in Africa are not without challenges. Issues such as political instability, regulatory hurdles, and local resistance to large-scale land acquisitions need careful navigation. However, the opportunities far outweigh the risks. The GCC’s proactive approach to addressing these challenges, combined with its financial muscle and strategic foresight, positions it as a pivotal player in Africa’s development trajectory.

In conclusion, the GCC’s expanding footprint in Africa is characterized by strategic investments across key sectors, bolstered trade relations, and a proactive approach to enhancing regional security and political influence. This multifaceted engagement is set to foster an era of closer economic and political ties, positioning the GCC as a leading player in Africa’s future development. The symbiotic relationship between the GCC and African nations is poised to usher in a new chapter of mutual growth and prosperity, underscored by shared interests and collaborative ventures.

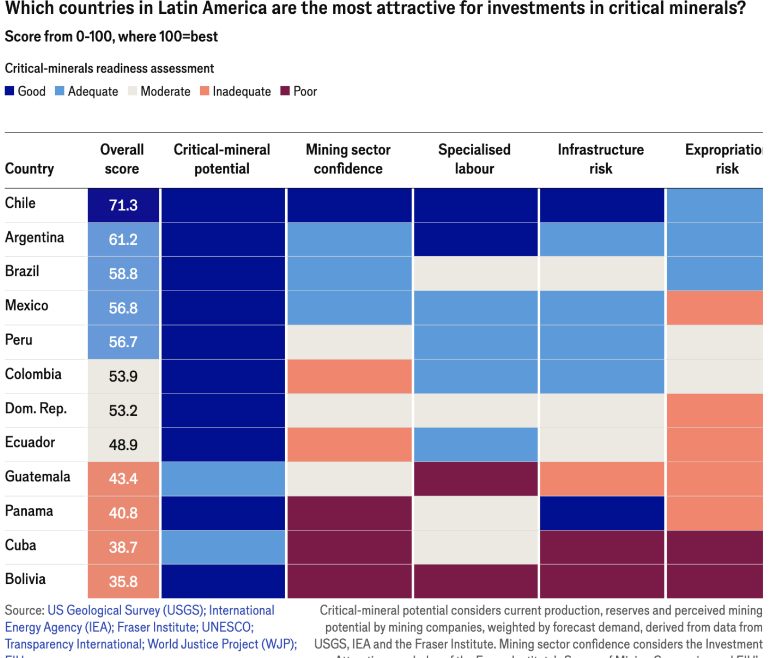

Critical Minerals in Latin America: Opportunities and Challenges

Overview

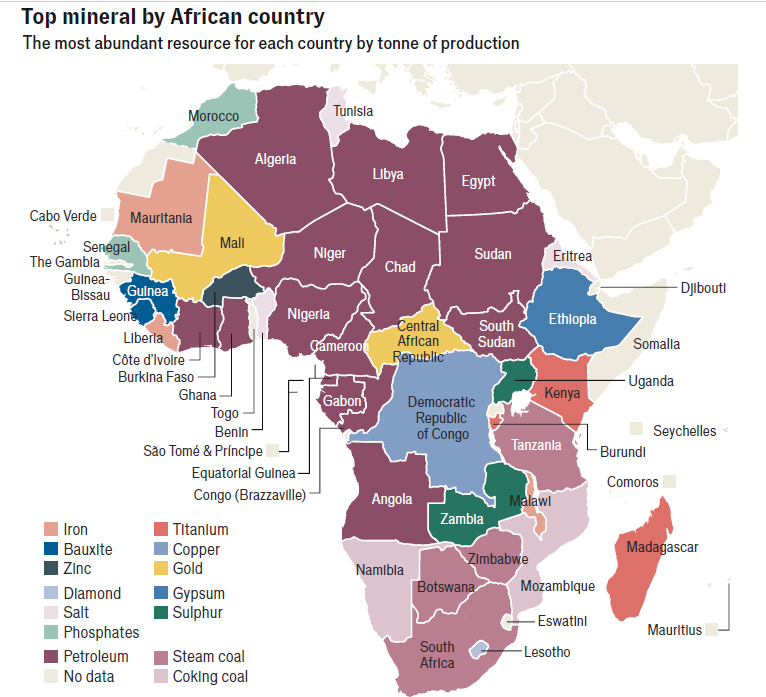

The competition for access to critical minerals has intensified among global powers, notably China, the US, and the EU, leading to a burgeoning interest in Latin America’s vast reserves of lithium, copper, nickel, and rare earth elements. These minerals are indispensable for the global energy transition and the advancement of technologies such as electric vehicles (EVs) and electricity-intensive artificial intelligence operations and data centers. Latin America, therefore, stands at a pivotal juncture, requiring substantial international mining investments to scale production and realize its developmental potential.

Current Landscape and Investment Potential

Latin America presents a mixed landscape of immense opportunities juxtaposed with significant challenges. Despite the region’s abundant mineral reserves, infrastructural deficiencies and high operational risks pose considerable hurdles. However, the region’s geographical distance from global conflict zones and its relatively low geopolitical risk make it an attractive investment destination for those seeking reliable supply chain partners.

Key Players and Readiness

Among Latin American nations, Chile, Argentina, and Brazil are the most prepared to attract critical mineral investments, as highlighted in the critical-minerals readiness heatmap. These countries exhibit a combination of robust infrastructure, legal stability, and a proactive stance towards foreign investment in mining. Conversely, Bolivia, Cuba, Guatemala, and Panama lag significantly, showing little immediate potential for improvement.

Chile Chile leads in readiness, benefiting from strong sectoral confidence, a steadfast commitment to the rule of law, and superior labor and infrastructure quality. However, regulatory concerns persist, particularly with cumbersome permitting processes and the current government’s statist approach to critical minerals, especially lithium. The country’s well-established mining sector, coupled with advanced technological capabilities and a stable economic environment, further bolsters its attractiveness to investors. Chile’s government has also been proactive in creating a conducive environment for mining investments, though the complexities in the regulatory framework remain a critical area needing reform.

Argentina Argentina has shown considerable promise, with extensive lithium reserves placing it at the forefront of the critical minerals market. The government has made significant strides in attracting foreign investments through favorable policies and incentives. However, challenges persist in the form of economic instability, inflation, and occasional political upheavals. Despite these obstacles, Argentina’s potential for growth in the critical minerals sector is substantial, driven by ongoing reforms and increasing international interest.

Brazil Brazil’s vast mineral wealth, particularly in nickel and rare earth elements, positions it as a key player in the region. The country has made efforts to streamline regulations and improve the business environment, but bureaucratic hurdles and socio-political issues remain deterrents. Brazil’s well-developed infrastructure and significant technological advancements in mining practices contribute to its readiness, though continued efforts are needed to address environmental and social concerns associated with mining operations.

Mexico and Peru Both Mexico and Peru possess significant mineral reserves and have made notable progress in attracting mining investments. Mexico’s regulatory environment has seen improvements, but security concerns and political uncertainties continue to pose challenges. Peru, with its rich deposits of copper and other critical minerals, has also worked towards enhancing its investment climate, though social unrest and regulatory inconsistencies remain issues. Despite these challenges, both countries offer substantial opportunities for growth in the critical minerals sector.

Colombia, Dominican Republic, and Ecuador These nations present higher risks for investors due to the lack of significant political commitment to enhance the regulatory environment and high potential for labor and social unrest, which are likely to persist through the forecast period of 2024-2028. Colombia’s potential is hindered by security issues and a challenging regulatory landscape. The Dominican Republic and Ecuador face similar hurdles, with political instability and insufficient infrastructure posing significant barriers to investment. Efforts to improve the business environment in these countries are ongoing, but substantial progress is needed to attract major mining investments.

Guatemala, Panama, Cuba, and Bolivia These countries are the least favorable for critical mineral investments. In Cuba and Bolivia, policies hostile to private investment are expected to remain unchanged. Bolivia’s significant lithium reserves are underutilized due to governmental policies that restrict foreign investment. Cuba’s approach towards private investment similarly dampens its potential despite its mineral wealth. Panama’s investment climate is further marred by an ongoing dispute with a Canadian operator over a major copper mine, adversely affecting its attractiveness. Guatemala’s regulatory environment and socio-political instability further hinder its potential to attract critical mineral investments.

Demand and Strategic Importance

The International Energy Agency projects a robust annual growth of over 6% in demand for critical minerals until 2030, underscoring the urgent need for increased mining investments in Latin America. The region holds more than half of the world’s lithium reserves, over a third of its copper, and nearly one-fifth of its nickel and rare earth metals. Despite this, Latin America’s share of global mineral production has been on the decline, primarily due to insufficient investment compared to other regions.

Challenges and Investment Climate

The underinvestment in Latin American mining projects can be attributed to unstable regulatory environments, labor and social unrest, and pervasive corruption. Nonetheless, the sheer magnitude of untapped reserves significantly offsets these challenges, positioning many Latin American countries as more favorable investment destinations than other major producers.

Country-Specific Insights

Chile Chile leads in readiness, benefiting from strong sectoral confidence, a steadfast commitment to the rule of law, and superior labor and infrastructure quality. However, regulatory concerns persist, particularly with cumbersome permitting processes and the current government’s statist approach to critical minerals, especially lithium. The country’s well-established mining sector, coupled with advanced technological capabilities and a stable economic environment, further bolsters its attractiveness to investors. Chile’s government has also been proactive in creating a conducive environment for mining investments, though the complexities in the regulatory framework remain a critical area needing reform.

Argentina Argentina has shown considerable promise, with extensive lithium reserves placing it at the forefront of the critical minerals market. The government has made significant strides in attracting foreign investments through favorable policies and incentives. However, challenges persist in the form of economic instability, inflation, and occasional political upheavals. Despite these obstacles, Argentina’s potential for growth in the critical minerals sector is substantial, driven by ongoing reforms and increasing international interest.

Brazil Brazil’s vast mineral wealth, particularly in nickel and rare earth elements, positions it as a key player in the region. The country has made efforts to streamline regulations and improve the business environment, but bureaucratic hurdles and socio-political issues remain deterrents. Brazil’s well-developed infrastructure and significant technological advancements in mining practices contribute to its readiness, though continued efforts are needed to address environmental and social concerns associated with mining operations.

Mexico and Peru Both Mexico and Peru possess significant mineral reserves and have made notable progress in attracting mining investments. Mexico’s regulatory environment has seen improvements, but security concerns and political uncertainties continue to pose challenges. Peru, with its rich deposits of copper and other critical minerals, has also worked towards enhancing its investment climate, though social unrest and regulatory inconsistencies remain issues. Despite these challenges, both countries offer substantial opportunities for growth in the critical minerals sector.

Colombia, Dominican Republic, and Ecuador These nations present higher risks for investors due to the lack of significant political commitment to enhance the regulatory environment and high potential for labor and social unrest, which are likely to persist through the forecast period of 2024-2028. Colombia’s potential is hindered by security issues and a challenging regulatory landscape. The Dominican Republic and Ecuador face similar hurdles, with political instability and insufficient infrastructure posing significant barriers to investment. Efforts to improve the business environment in these countries are ongoing, but substantial progress is needed to attract major mining investments.

Guatemala, Panama, Cuba, and Bolivia These countries are the least favorable for critical mineral investments. In Cuba and Bolivia, policies hostile to private investment are expected to remain unchanged. Bolivia’s significant lithium reserves are underutilized due to governmental policies that restrict foreign investment. Cuba’s approach towards private investment similarly dampens its potential despite its mineral wealth. Panama’s investment climate is further marred by an ongoing dispute with a Canadian operator over a major copper mine, adversely affecting its attractiveness. Guatemala’s regulatory environment and socio-political instability further hinder its potential to attract critical mineral investments.

Strategic Outlook

Latin America’s potential in the critical minerals sector is vast but requires strategic investments and regulatory reforms to be fully realized. The region’s untapped reserves represent a significant opportunity for global investors, provided the challenges of regulatory instability, infrastructural inadequacies, and socio-political risks can be effectively managed. As global demand for critical minerals continues to surge, Latin America’s strategic importance on the global stage is set to increase, making it a focal point for future mining investments and geopolitical interest.

To capitalize on these opportunities, Latin American countries must prioritize improving their regulatory frameworks, investing in infrastructure, and ensuring political stability. Strengthening partnerships with international investors and fostering a conducive business environment will be crucial in transforming the region into a leading hub for critical minerals. The success of these efforts will significantly impact the global supply chain for critical minerals and contribute to the advancement of sustainable technologies worldwide.

By leveraging its vast resources and addressing the existing challenges, Latin America has the potential to become a cornerstone of the global supply chain for critical minerals, driving forward the energy transition and technological advancements that are crucial for a sustainable future.

Comprehensive Country Analysis

Detailed country analysis provides essential insights into political, economic, and market-moving topics. This service includes:

- Global and regional outlooks on politics, economics, and significant market trends.

- Daily insights into developments affecting future outlooks.

- Executive summaries of medium-term country forecasts covering political and economic landscapes for approximately 200 countries.

- Long-term forecasts on structural trends shaping around 80 major economies.

- Industry analysis for 26 sectors across approximately 70 markets.

- Commodity forecasts covering supply, demand, and prices of 25 critical goods.

- Extensive macroeconomic and industry data, including historical trends and future forecasts.

- Proprietary ratings on the business environment.

- Thematic analysis on key issues expected to shape the global outlook.

This analysis helps organizations plan and operate effectively, providing expansive coverage, robust data, and non-biased, rigorously researched forecasts. The service aims to challenge consensus and offer nuanced insights into politics, policy, and the economy.

For More Information:

If you would like more specific information about our Market Analysis service or details from other countries and continents, please contact [email protected].

The information in this summary has been gathered from multiple sources, including:

- Global real GDP growth and projections.

- Analysis of monetary policy adjustments.

- Geopolitical tensions and economic fragmentation.

- Inflation trends and forecasts.

- Long-term economic trends, including the impact of climate change and AI.

- Comprehensive country analysis.

© 2024. All rights reserved. Reproduction and transmission @Borderless Consulting

“The global economic outlook for 2024 shows surprising resilience with a forecasted real GDP growth of 2.5%, matching the growth rate of 2023 despite high interest rates and geopolitical challenges. This strength is driven by an upward revision in the US growth forecast to 2.2%, alongside positive adjustments for several European economies and Brazil. However, geopolitical tensions, such as conflicts in the Middle East and Russia’s invasion of Ukraine, continue to pose risks.

Inflation remains a concern, projected to settle at higher levels than pre-pandemic trends due to tight labor markets, demographic shifts, and supply chain reconfigurations. Monetary policy will see limited loosening, with the US Federal Reserve delaying rate cuts until September 2024, while the European Central Bank and Bank of England are expected to act earlier.

Over the next five years, the global economy will face challenges from climate change and AI, which are likely to widen the gap between developed and developing economies. Despite these headwinds, countries like India and Mexico are poised for robust growth, driven by strong domestic factors and favorable global trends.

For comprehensive insights and detailed country-specific analysis, our service offers extensive coverage and data-driven forecasts, enabling organizations to navigate the complexities of the global economic landscape effectively.”

For more specific information or details from other countries and continents, please contact [email protected].

Julio Verissimo

President & CEO

Borderless Consulting

Indulge yourself in the mesmerizing world of Julio Verissimo Live Show, an extraordinary showcase of talent, passion, and artistic brilliance. This captivating event promises an unforgettable experience, inviting audiences to immerse themselves in a symphony of sights and sounds that transcend the ordinary.

At the heart of Julio Verissimo Live Show lies a dedication to excellence, where each performance is meticulously crafted to evoke emotion, ignite the imagination, and leave a lasting impression on all who witness it. From the stirring melodies of live music to the graceful movements of dance, every aspect of this show is infused with a sense of purpose and meaning.

Step into the virtual realm of Julio Verissimo Live, where innovation meets artistry in perfect harmony. Through cutting-edge technology and immersive visuals, audiences are transported to a world of boundless possibilities, where the limits of creativity are pushed to new heights.

But beyond its technical brilliance, Julio Verissimo Live Show embodies a deeper ethos—a commitment to fostering connection, fostering connection, and celebrating the rich tapestry of human experience. It is a testament to the power of art to unite, inspire, and uplift, transcending barriers of language, culture, and geography.

As you embark on this enchanting journey with Julio Verissimo Live Show, prepare to be moved, inspired, and transformed. Allow yourself to surrender to the magic of the moment, as you witness the extraordinary talents of Julio Verissimo and his ensemble cast. For in this wondrous spectacle, you will find not only entertainment but also a profound reminder of the beauty and wonder that abound in our world.

Experience Julio Verissimo Live Show and embark on a voyage of discovery, creativity, and wonder that will stay with you long after the final curtain falls. Join us as we celebrate the power of art to illuminate, uplift, and inspire the human spirit.

Furthermore, it is with great pleasure and excitement that I announce a new chapter in our journey of artistic collaboration. In a commitment to expand our reach and deepen our impact, we are proud to unveil our partnership with Hispanic Public Media and DW Hispanic in Mexico.

This collaboration represents a union of shared values and aspirations, as we collectively strive to promote cultural exchange, diversity, and inclusivity through the power of media and the arts. With a steadfast dedication to excellence and integrity, Hispanic Public Media and DW Hispanic in Mexico have established themselves as beacons of journalistic integrity and cultural enrichment, resonating with audiences across the globe.

By joining forces with these esteemed organizations, we aim to amplify our message and extend the reach of Julio Verissimo Live Show to even more audiences, both within the Hispanic community and beyond. Together, we will harness the transformative power of art and storytelling to foster understanding, empathy, and connection in an increasingly interconnected world.

This partnership heralds a new era of cooperation and collaboration, where diverse voices come together in harmony to celebrate our shared humanity and embrace the richness of our cultural heritage. Through joint initiatives, cross-promotional efforts, and collaborative projects, we will pave the way for greater synergy and mutual enrichment, creating opportunities for growth and innovation for all parties involved.

As we embark on this exciting journey together, I am filled with optimism and anticipation for the countless possibilities that lie ahead. Together with Hispanic Public Media and DW Hispanic in Mexico, we will continue to uphold the highest standards of excellence and strive to make a meaningful difference in the lives of our audiences, inspiring, enlightening, and empowering individuals across borders and boundaries.

I invite you to join us on this remarkable adventure as we embark on a shared mission to promote understanding, celebrate diversity, and build bridges of connection and cooperation that transcend language, culture, and geography. Together, we will write the next chapter in the story of Julio Verissimo Live Show—a story of collaboration, innovation, and boundless creativity.

Stay tuned for more updates and announcements as we embark on this exciting new journey together.

Visit https://liveshow.bodlsc.com/ and prepare to be dazzled by Julio Verissimo

“In the tapestry of cultural collaboration, our partnership with Hispanic Public Media and DW Hispanic in Mexico threads together with Julio Verissimo Live Show a vibrant narrative of unity, diversity, and shared vision. Together, we weave the fabric of understanding, bridging hearts and minds through the transformative power of art and storytelling.”

Julio Verissimo

President & CEO

Borderless Consulting

In case you missed latests podcasts

Continuing the odyssey on this podcast, “Exploring Montenegro’s Economic Resilience: Strategic Investments and Insights,” beckons with the promise of unraveling the secrets to prosperity in the face of adversity. Under the sage guidance of Julio Verissimo and the esteemed presence of special guest Arben Jakupi, we embark on a voyage through the intricacies of economic resilience. Together, we shall navigate the turbulent seas of uncertainty, armed with the wisdom of strategic investments and fortified by the resilience of the human spirit. Anticipation mounts as we eagerly await the revelation of the auspicious date for this enlightening discourse and be part of a community dedicated to shaping a brighter future. EconomicResilience #InvestmentStrategies #MontenegroEconomy #StrategicInsights #ProsperityPathways

Prepare to be captivated by the podcast, “Vision and Risk-Taking: Paving the Way to Environmental Sustainability,” where Julio Verissimo, our guiding beacon of wisdom, leads us on a transformative journey towards a greener tomorrow. Joined by the illustrious John Graham, we embark on an expedition of visionary thought, daring to challenge the status quo and pioneer solutions for a sustainable future. Let us unite in this noble endeavor, harnessing the power of collective insight to forge a path towards environmental stewardship that knows no bounds and become a catalyst for change.SustainabilityJourney. #EnvironmentalVisionaries #GreenFuture #EcoLeadership #SustainableSolutions

Subscribe our channels

On Linkedin

On Instagram

On Twitter X

We're teaming up with Hispanic Public Media and DW Hispanic MX to bring you an unforgettable experience! Join us as we embark on a journey of cultural collaboration and celebration through Julio Verissimo Live. Stay tuned https://t.co/hbXNKaYoGD

— Julio Verissimo (@Julio_Verissimo) May 5, 2024